Trying to navigate the world of health savings can be confusing, especially with acronyms like FSAs and HSAs flying around. But fear not! This guide will break down exactly what Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) are, how they work, and which one might be the better fit for you.

The Bottom Line Up Front: Both FSAs and HSAs let you save pre-tax dollars to cover qualified medical expenses, reducing your taxable income. However, they differ in eligibility, contribution limits, rollover options, and potential use as a retirement savings tool.

Understanding FSAs (Flexible Spending Accounts):

Imagine a special account you contribute pre-tax dollars to throughout the year. This money is then specifically used to pay for eligible medical expenses for you, your spouse, and dependents. Think of it as a healthcare savings account with a “use it or lose it” rule.

Key Features of FSAs:

- Employer-based: Offered by your employer as part of a cafeteria plan.

- Contribution Limits: Set annually by the IRS and adjusted for inflation. The limit for 2023 is $3,050.

- Use It or Lose It: Unused funds at year-end are generally forfeited, though some plans offer grace periods or contribution carryovers.

- Eligible Expenses: Cover a wide range of medical costs like deductibles, copays, prescriptions, and even feminine hygiene products.

Important FSA Considerations:

- Not Portable: You can’t take your FSA with you if you leave your job.

- Careful Planning Needed: Estimate your medical expenses for the year to avoid forfeiting unused funds.

HSAs (Health Savings Accounts): A Tax-Advantaged Powerhouse

HSAs offer a more flexible and potentially powerful option compared to FSAs. However, eligibility comes with a twist: you must be enrolled in a high-deductible health plan (HDHP) to qualify.

Who Can Have an HSA?

- Not covered by Medicare

- Not claimed as a dependent on someone else’s tax return

- Enrolled in a high-deductible health plan (HDHP) with no other non-HDHP coverage (except permitted exceptions like dental or vision insurance)

HSA Advantages:

- Individual or Employer-based: You can set up your own HSA or participate in an employer-sponsored plan.

- Higher Contribution Limits: Compared to FSAs, HSAs offer higher contribution limits for 2023: $3,850 for self-only coverage and $7,750 for family coverage. Those aged 55 and over can contribute an additional $1,000.

- Rollover Feature: Unlike FSAs, unused funds in your HSA roll over year after year, allowing your savings to grow.

- Triple Tax Advantage: Contributions are tax-deductible, earnings on investments within the HSA grow tax-free, and qualified medical expense distributions are tax-free.

- Potential Retirement Powerhouse: HSAs can function as a long-term savings vehicle for future medical expenses. Even if used for non-medical reasons after age 65, distributions are taxed only as income, not penalized.

Things to Remember About HSAs:

- HDHP Requirement: You must be enrolled in an HDHP to qualify for an HSA. HDHPs typically have lower monthly premiums but higher deductibles.

- Plan for Medical Expenses: While HSAs can be a retirement tool, they are still meant for medical expenses. You’ll pay a 20% penalty on non-medical distributions before age 65.

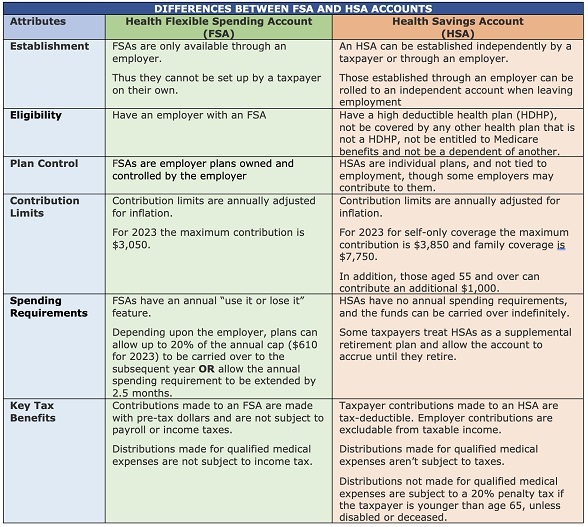

FSA vs. HSA: A Side-by-Side Comparison

Choosing Between FSAs and HSAs

The best choice depends on your individual circumstances. Here’s a quick guide:

- Good for FSAs: Those with predictable medical expenses who want a way to save pre-tax dollars for healthcare costs.

- Good for HSAs: Individuals with high-deductible health plans (HDHPs), those looking to save for future medical expenses and potential retirement savings, and people who are disciplined enough to manage an HSA as a triple tax-advantaged account.

Ultimately, by understanding the nuances of FSAs and HSAs, you can make an informed decision that best suits your health needs and financial goals. We recommend consulting with a financial advisor to determine which option is the right fit for you.

If you have any questions about FSAs, HSAs, or other tax-saving health plans, our office is here to help! Contact us today to schedule a consultation.